When should you consider a Roth Conversion?

Learn about Roth IRA conversions, weighing the pros and cons, and determine if it's a fit for your financial strategy in 2024.

Roth IRA conversions can be a smart financial move for some individuals. However, before making this decision, it’s important to understand the basics, benefits, and potential drawbacks. This guide will explore all aspects of Roth conversions, discuss key factors to consider, and provide a step-by-step method to determine if a Roth conversion is right for you.

Understanding Roth Conversions

A Roth conversion involves moving funds from a traditional IRA or 401(k) into a Roth IRA. This strategic move allows you to pay taxes on the converted funds now, so you can enjoy tax-free withdrawals during retirement. The funds converted will be subject to income tax in the year of the conversion. Roth IRAs are unique because contributions are made with after-tax dollars. This means you’ve already paid taxes on the funds contributed. The advantage is that all qualified withdrawals, including potential investment gains, are tax-free. Additionally, Roth IRAs have no required minimum distributions (RMDs) during the account holder’s lifetime, providing greater flexibility in retirement planning.

The Benefits of Roth Conversions

- Tax-Free Withdrawals: Enjoy tax-free withdrawals during retirement, potentially saving a significant amount in taxes.

- No Required Minimum Distributions: Roth IRAs do not require you to take minimum distributions, allowing your funds to grow tax-free indefinitely.

- Estate Planning: Leave a lasting legacy of tax-free wealth transfer for future generations.

The Drawbacks of Roth Conversions

- Conversion Taxes: Converting funds results in a substantial tax bill in the year of the conversion.

- Impact on Current Tax Bracket: Roth conversions are considered taxable income, which can push you into a higher tax bracket.

- Five-Year Rule: To qualify for tax-free withdrawals, you must have held the account for at least five years.

Factors to Consider Before a Roth Conversion

Evaluating your current and future tax rates is crucial. If you anticipate being in a higher tax bracket during retirement, a Roth conversion can be advantageous. Conversely, if you expect to be in a lower tax bracket, it may be more beneficial to keep your funds in a traditional retirement account. The longer you have until retirement, the more time your converted funds have to grow and potentially offset the upfront tax burden. If retirement is imminent, the benefits of a Roth conversion may be limited.

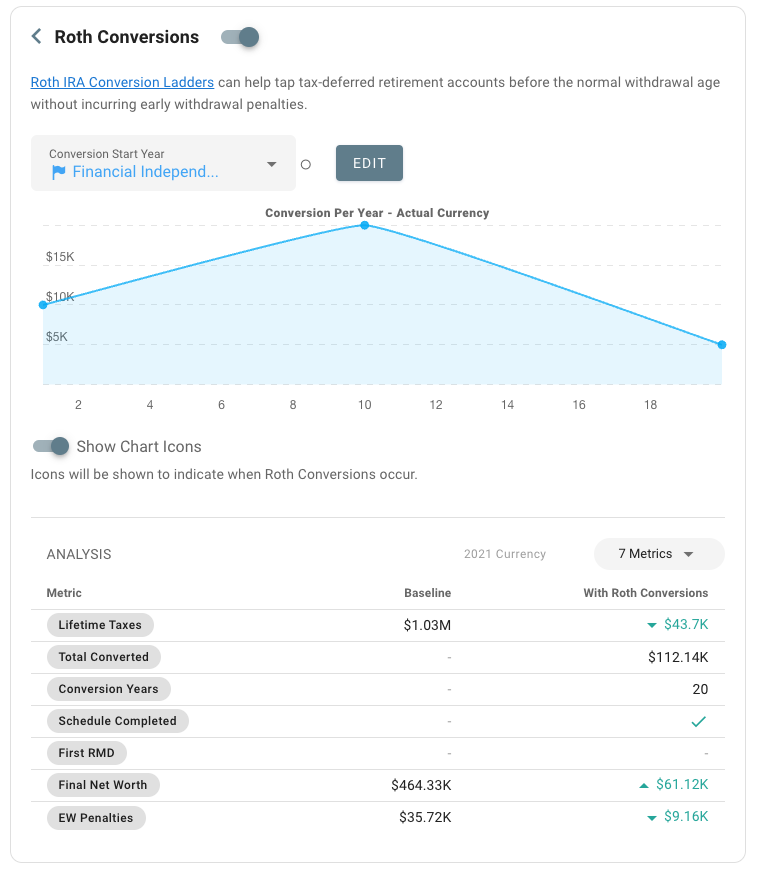

Roth conversion planning in ProjectionLab.

If you’re planning to retire early, understanding how to access your retirement funds without penalties is essential. One effective strategy is utilizing Roth Conversion Ladders, which involve converting traditional IRA or 401(k) funds to a Roth IRA incrementally over several years. This approach allows you to access funds early while avoiding the usual early withdrawal penalties. For more information on Roth Conversion Ladders and other strategies, check out: How to Access Retirement Funds Early by Mad Fientist. It offers valuable insights that complement your Roth conversion planning.

Guide to Roth Conversion

Step 1: Check Your Tax Bracket

Why it Matters: The 24% tax bracket presents a significant opportunity for taxpayers to lock in a lower rate before the Tax Cuts and Jobs Act (TCJA) expires in 2026, which will increase most tax rates. The 24% rate will see the largest increase, rising by 4% to 28%, which equates to an additional $4,000 per $100,000 of income. While it’s possible to consider trying to benefit from the smaller difference between the current top rate of 37% and the future rate of 39.6%, doing so involves a considerable current tax expense. The expiration of the TCJA makes the 24% bracket a strategic point for financial decisions like conversions, due to its balance of accessibility and impact.

How to Do It:

- Find Your Taxable Income: Look at the last line on page 1 of your 2023 Form 1040.

- Estimate 2024 Income: Consider any raises, business profits, or additional deductions.

- Identify the 24% Bracket Limit: For 2024, a single filer can have up to $191,950 in income before moving to a higher bracket. For those married filing jointly, the limit is $383,900.

- Calculate Your Conversion Amount: Subtract your estimated 2024 income from $191,950 (single) or $383,900 (married filing jointly). If positive, this is the maximum amount you should consider converting.

Example: If your estimated 2024 taxable income is $160,000 (single), you can convert up to $31,950 to stay within the 24% bracket.

Step 2: Determine Tax-Cost Efficiency

Why it Matters: You achieve tax-cost efficiency when the future tax savings from a Roth conversion outweigh the growth in tax cost if you leave your money in a traditional IRA.

How to Do It:

- Calculate Current Tax Cost: For example, converting $10,000 at a 24% tax rate costs $2,400.

- Estimate Future Value: Assume your $10,000 grows at 7.2% annually for 10 years, resulting in $20,060.

- Predict Future Tax Bracket: If you expect to be in the 28% bracket in the future, your tax cost will be $5,616.80.

- Compare Growth Rates: Determine if the future tax cost growth (in this case, 8.84%) exceeds your investment growth rate (7.2%).

Example: If the tax cost grows faster than your investment, a Roth conversion is tax-efficient.

Step 3: Consider Additional Factors

Why it Matters: This step ensures you’re considering personal circumstances that might affect your decision.

Questions to Ask:

- Future Tax Rate: Will your future tax rate be lower? If yes, a Roth conversion might not be beneficial.

- Need for Funds: Do you need this money within five years? If so, avoid conversion to prevent penalties.

- Heirs and Long-Term Care: Do you have heirs or long-term care needs? If yes, a Roth conversion can preserve more wealth for these purposes.

- Cash to Pay Taxes: Do you have the cash to pay taxes now? If not, think carefully about proceeding.

Example: If you plan to retire in a lower tax bracket, it might not make sense to convert now.

How to Do a Roth Conversion

Steps to Convert to a Roth IRA:

- Evaluate Your Current Retirement Accounts: Review your existing retirement accounts, such as traditional IRAs and 401(k)s, and assess the funds you would like to convert.

- Calculate Conversion Taxes: Determine the potential tax implications by consulting with a tax professional or using an online tax calculator.

- Complete a Conversion Request: Contact your financial institution or brokerage firm to initiate the conversion process. They will guide you through the necessary paperwork and provide instructions on how to transfer the funds.

- Consider Partial Conversions: If converting all of your funds would result in a hefty tax bill, consider gradually converting smaller amounts over several years to mitigate the tax impact.

- Ensure Proper Reporting: When tax season arrives, ensure that you report the conversion properly on your tax return to avoid any penalties or audits.

Dealing with Conversion Taxes: If you anticipate a significant tax bill from the conversion, plan ahead and have sufficient funds set aside to cover it. Consider consulting with a tax professional who can help you navigate the tax implications and develop a strategy to minimize the impact on your finances.

Deciding whether to do a Roth conversion requires careful evaluation of your individual financial circumstances and goals. While advantageous for individuals in specific situations, Roth conversions may not be the right choice for everyone. By understanding the basics, considering the benefits and drawbacks, and analyzing the factors that apply to your situation, you can make an informed decision that aligns with your long-term financial objectives.

If you’re considering a Roth conversion, ProjectionLab can help you model different scenarios and make the best decision for your financial future. Our comprehensive financial planning tool allow you to see the potential tax impacts and long-term benefits of converting to a Roth IRA. Get started with ProjectionLab today and take control of your retirement planning! For more insights on Roth conversions, watch our video on roth conversions in ProjectionLab

Disclaimer: The content, tools, and resources on ProjectionLab.com are intended solely for informational and educational purposes and should not be construed as professional financial or investment advice. Our materials are designed to provide general guidance and are based on the input and data provided by users. ProjectionLab makes no guarantee of the accuracy, completeness, or applicability of this content to individual circumstances. Effective financial planning and investment involve comprehensive consideration of a wide array of personal financial factors. The tools and resources available on ProjectionLab are aimed at helping users develop an understanding of their financial trajectory. However, they should not be solely relied upon for creating a complete financial plan. We strongly recommend consulting a financial services professional who can provide personalized advice based on your unique financial situation before making any significant financial decisions. While we endeavor to keep the information on ProjectionLab current and accurate, the content may differ from that found on other financial institutions, service providers, or specific product sites. All content and tools on ProjectionLab are provided without any guarantees or warranties of any kind.